Technology and International Stock Exchange Listings for US companies

An IPO is often the most important capital markets and wealth creation event in a corporate life cycle. Unmatched access to capital at a lower cost is a clear benefit in favour of an IPO, along with corporate branding opportunities and a host of other benefits.

Companies consider three things when choosing a listing location—the actual out-of-pocket costs for establishing and maintaining the listing, the effects on valuation and liquidity, and the nonfinancial benefits.

However, before addressing these substantial IPO listing considerations a US private company considering an IPO, with a value of less than US$1 billion must realise that it is almost certainly too small to list successfully in the USA these days. Moreover, the competitiveness of the US public market has been seriously challenged in recent years as indicated below:

- The age of companies at time of a US IPO has increased (from ~6.5 to ~10.5 years);

- The annual number of US IPOs decreased (from ~400 to ~100);

- The valuation of US IPOs has increased more than 6x.

IPOs in the United States typically have significantly high expenses. Legal and accounting fees, printing, brokerage charges to raise the capital, insurances, director fees and other related expenses are substantially higher than in many other countries.

In particular, companies trying to go public in the US are prone to litigation and enormous expense. Floats are fewer but larger, because by the time the company reaches a stage where it can afford to list, it is mature. For a technology company to list on Nasdaq, it needs to be circa US $ 1 billion to get any traction. Conversely, listing overseas, for example on the Australian Securities Exchange (ASX), can present itself as the ideal market for technology companies valued under US$ 1billion.

The Securities and Exchange Commission (SEC) regulatory compliance expenses are also significantly higher than internationally. These expenses can become very material for companies having a post-IPO market value of less than US$ 1billion. It is often felt that in the United States a small company has to pay too much in fees and discounts when it sells its stock to the public.

Destinations for US companies under US 1billion in value.

There are two self-contained regions that are popular with US companies wishing to go public, outside of the USA, which are Europe and Asia Pacific. However, Australia also represents an increasingly popular destination.

Why are foreign companies listing in Australia?

Australia’s large fast -growing pension pool, main board listing and earlier entry to globally recognised indices makes the ASX the exchange of choice for international companies. To date, more than 280 international companies are listed on ASX.

Access to growth capital is the major attraction of the ASX for international listings and this article explains how and why this is the case.

Australia has the fourth largest pension pool globally and also one of the fastest growing. Superannuation assets total A$2.6 trillion and this is predicted to grow to A$9.5 trillion by 2035.

The reason behind the size of the Australian pension pool is the compulsory superannuation system introduced by the Australian Federal Government in 1992. The sheer weight of this pool, where a large percentage is mandated to invest directly in ASX-listed securities, makes the Australian market an attractive venue for international companies looking to access capital for growth.

Why the ASX?

In addition to capital, an ASX listing offers a number of other benefits for an international company looking at global public markets. These include a highly active exchange, a main board listing and earlier entry to globally recognised indices.

The ASX is a very active exchange, typically exceeding 120 initial public offerings (IPOs) a year and trading volumes averaging $5.6 billion on a daily basis.

The ASX’s main board listing, provides a globally recognised robust regulatory environment and access to the full breadth of investors from retail to global institutions. Access to the main board for earlier-stage growth companies is in contrast to a junior board listing, typical in other jurisdictions, where full access to the investor base can be more limited.

Often, institutional investor mandates stipulate fund managers limit their investment to a globally recognised exchange and not extend to many secondary boards or smaller main boards, examples of which are the AIM market in the UK, TSX-V in Canada, GEM in Hong Kong and Catalist in Singapore.

Index inclusion is another key factor. ASX has two globally recognised S&P indices, the S&P/ASX 300 and S&P/ASX 200. The importance of index inclusion to a listed company is the access this provides to institutional investment, both passive and active.

Institutional mandates are typically mandated to a recognised index and when a company enters an index it will lead to extended investment reach, both domestic and global, as that index weight increases.

The institutional investment in the S&P/ASX 200 index is comprised of about 45 per cent from global asset managers and 55 per cent Australian, meaning companies listed on ASX can have a register of globally recognised investors at an earlier stage than other markets.

Achieving global reach.

In the past five years there has been an increase in the number of international companies listing on ASX. It is an attractive listing venue for international companies from a number of different markets but these can be broadly characterised by (i) companies located in a constrained home capital market and (ii) those where size can cause them to be lost in their home market.

Getting lost in your home market.

In contrast, companies from large capital markets such as the United States also benefit from the Australian market dynamics. The size of the US public markets means that earlier-stage companies, with annual revenues below US$100 million or valued at US$1 billion market capitalisation or less, struggle to foster investor attention.

The US private markets are the most active globally and feature high-profile companies such as Uber, Spotify and Airbnb who have held off listing until they are well beyond that size. As a result, there is a whole generation of companies that would prefer to access the public markets, versus private funding, at an earlier stage, but their home exchange cannot support this.

ASX is bridging the gap for companies in these larger markets who would like to use the public markets to raise growth capital and can use ASX as a springboard to reach a size where they would attract attention in their home market.

There are currently 47 US companies listed on ASX. The US cohort of companies range across industries but the recent trend has been in the software and technology sector.

Why are technology companies listing on the ASX?

Technology is the fastest growing sector on the ASX.

Numerous growth-stage technology companies from Australia, the Asia-pacific, the US, Europe and Israel are successfully listing on the ASX with good valuations and traction for scale. These listings illustrate a clear trend which has emerged, that is the ASX is increasingly being used by technology companies as either a stepping stone to a future dual listing on other exchanges or as a long-term listing venue.

Many young technology companies are listed on ASX. Usually, in the US and other major markets, such young companies are considered as mid-stage or late-stage pre-IPO growth firms, and they seek venture capital as Series B, Series C, Series D, etc.

However, in Australia, retail investors accept investing in high-risk young firms that are still figuring-out their growth-model.

The key advantage for investors is that growth in the ASX technology sector, in both domestic and foreign companies, expands the universe of available investing options.

The ASX – A baby Nasdaq.

The ASX is targeting smaller tech companies that would not be able to list on the Nasdaq.

The ASX is positioning itself as a late-stage venture capital funding market with companies that have de-risked their model, have proven their revenue and are looking to scale their businesses and potentially go public to provide liquidity for their shareholders and acquisition currency.

Final Thoughts.

If a company is considering an IPO it will have recognised that it is one of the most important capital markets and wealth creation event in its’ corporate life cycle. That recognition should have extended to all of the factors that will influence the likely success of an IPO. Listing location should be high on that list of factors when formulating an IPO strategy. BlueMount Capital are experts in developing appropriate strategies and facilitating an IPO listing, particularly in Australia. BlueMount would welcome discussing with you how the capital raising opportunity which Australia represents can add value to your listing potential.

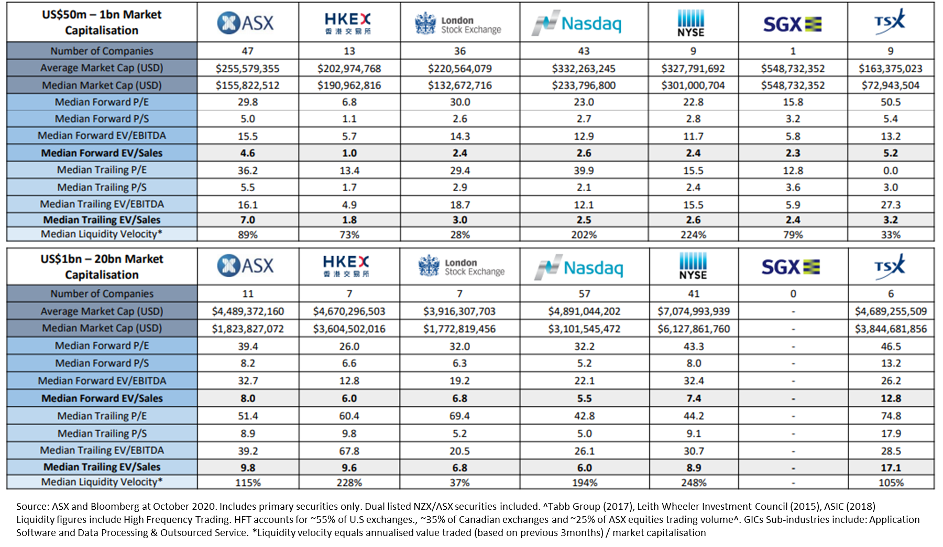

Data illustrating the ASX opportunity.

Technology valuations on the ASX.

Examples of US technology companies listed on ASX

Top Ten Technology “Unicorns” on the ASX

About BlueMount Capital

BlueMount Capital specialises in bringing US companies to the ASX, and has an office in Los Angeles to service its American clients

Len McDowall Alex Chen

Managing Director Director and USA representative

Level 32 200 George St 1055 W 7th, 33rd Floor, Penthouse

Sydney 2000 Australia Los Angeles CA 90017 USA

Telephone +61 2 8277 4112 Telephone +1 212 470 6997

Email sydney@bluemountcapital.com Email losangeles@bluemountcapital.com